SMM November 11:

Highs are hard to sustain! Although the pace of production increases for domestic primary aluminum billets continued in October, as the off-peak and peak seasons transition, weakening downstream orders are gradually transmitting upstream, and the operating rate for aluminum billets is expected to retreat from highs in November. In October, aluminum billet processing fees in major domestic consumption regions remained stable, and downstream operating performance managed to hold up during the seasonal transition, helping the aluminum billet operating rate continue to rise, supported by the inertia from the policy favoring liquid aluminum alloying. However, entering November, persistently high SHFE aluminum prices are suppressing some downstream demand; weakening downstream orders are gradually affecting upstream aluminum billet producers. Processing fees are expected to remain under pressure, some enterprises already have marginal production cut plans, and aluminum billet production across provinces is expected to decrease to varying degrees in November. The daily average production of domestic primary aluminum billets in October held steady MoM at around 51,000 mt/day, and is forecast to drop back slightly to 50,000 mt/day in November.

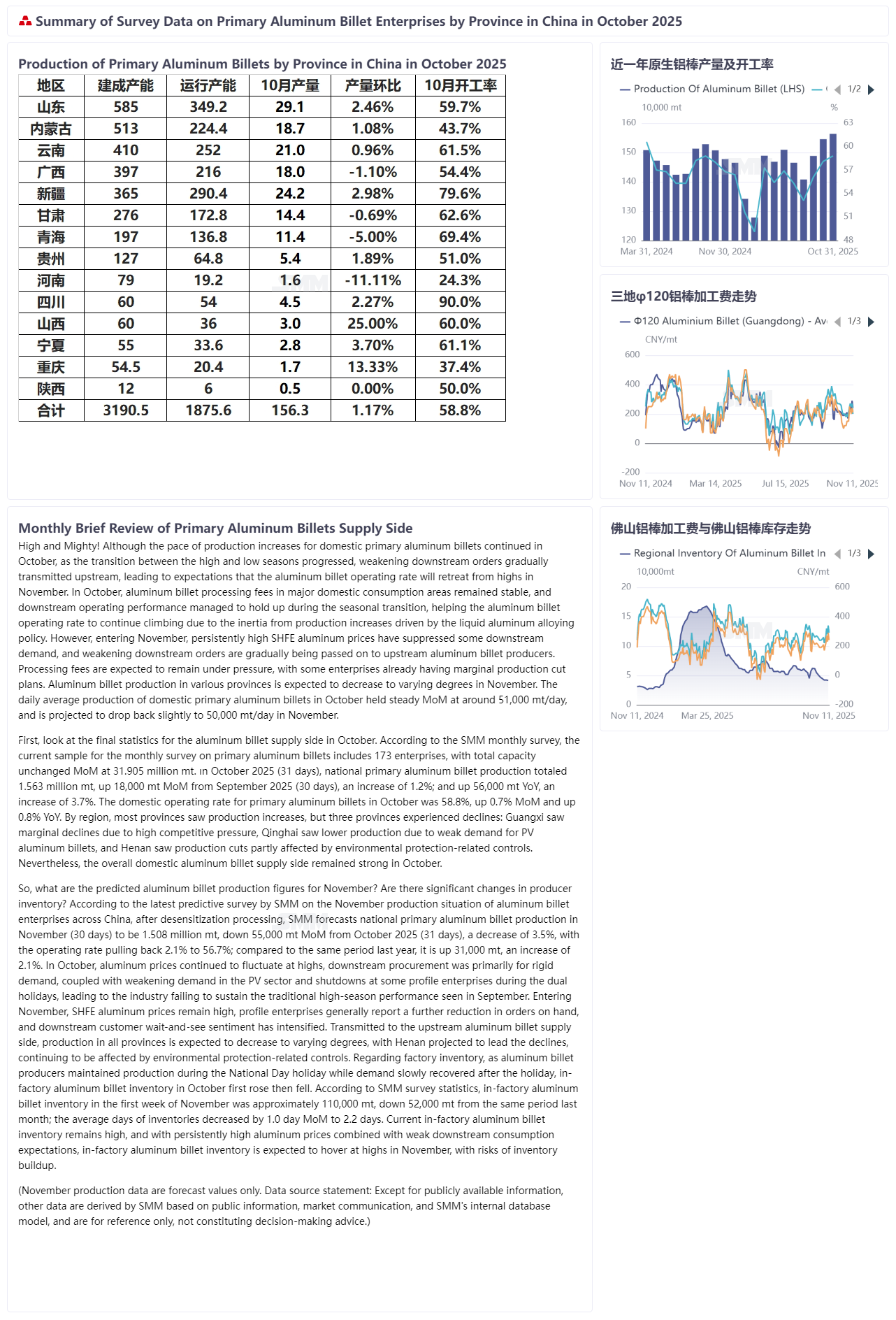

First, look at the final statistics for the aluminum billet supply side in October. According to the SMM monthly survey, the current sample for the monthly primary aluminum billet survey comprises 173 enterprises, with total capacity unchanged MoM at 31.905 million mt. National primary aluminum billet production in October 2025 (31 days) was 1.563 million mt, up 18,000 mt (or 1.2%) MoM from September 2025 (30 days), and up 56,000 mt (or 3.7%) YoY. The domestic operating rate for primary aluminum billets in October was 58.8%, up 0.7% MoM and up 0.8% YoY. By region, production increased in most provinces, but decreased in three: Guangxi saw marginal decline due to high competitive pressure, Qinghai due to weak demand for PV aluminum billets, and Henan was partly affected by environmental protection-related controls. Nonetheless, the national aluminum billet supply side overall held up well in October.

So, what are the predicted aluminum billet production figures for November? Are producer in-factory inventory changes significant? Based on SMM's latest predictive survey of aluminum billet enterprises across provinces for November production, desensitized, SMM forecasts national primary aluminum billet production in November (30 days) at 1.508 million mt, down 55,000 mt (or 3.5%) MoM compared to October 2025 (31 days). The operating rate is expected to pull back 2.1% to 56.7%, while increasing 31,000 mt (or 2.1%) YoY. In October, aluminum prices continued to fluctuate at highs, downstream procurement was primarily for rigid demand, coupled with weakening demand from the PV sector and holiday shutdowns at some profile enterprises during the National Day-Mid-Autumn Festival period, leading the industry to fail to sustain the traditional peak season performance seen in September. Entering November, SHFE aluminum prices remain high, profile enterprises generally report further reduction in orders on hand, and downstream customer wait-and-see sentiment has intensified. Transmitting to the upstream aluminum billet supply side, production across provinces is expected to decrease to varying degrees, with Henan anticipated to see the largest decline, continuing to be affected by environmental protection-related controls. Regarding in-factory inventory, as aluminum billet producers maintained production during the National Day holiday while demand recovered slowly after the holiday, in-factory inventory for aluminum billets in October first rose then fell. According to SMM survey statistics, domestic aluminum billet in-factory inventory in the first week of November was about 110,000 mt, down 52,000 mt from the same period last month; the average days of inventories decreased 1.0 day to 2.2 days compared to the same period last month. Current aluminum billet in-factory inventory remains high, and with persistently high aluminum prices combined with weak downstream consumption expectations, aluminum billet in-factory inventory in November is expected to hover at highs, with inventory buildup risks. (The November production data is only a forecast. Data Source Statement: Except for publicly available information, other data are processed by SMM based on public information, market communication, and SMM's internal database model, and are for reference only, not constituting decision-making advice.)